Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

A Confident Market Heading into Fall

The Johnson County housing market continues to show solid momentum as we move through the second half of 2025. Both home prices and sales activity are trending upward, reflecting ongoing confidence among buyers and sellers alike.

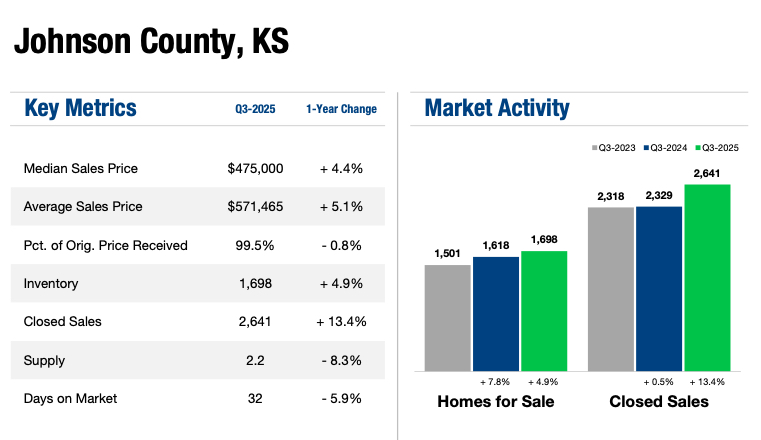

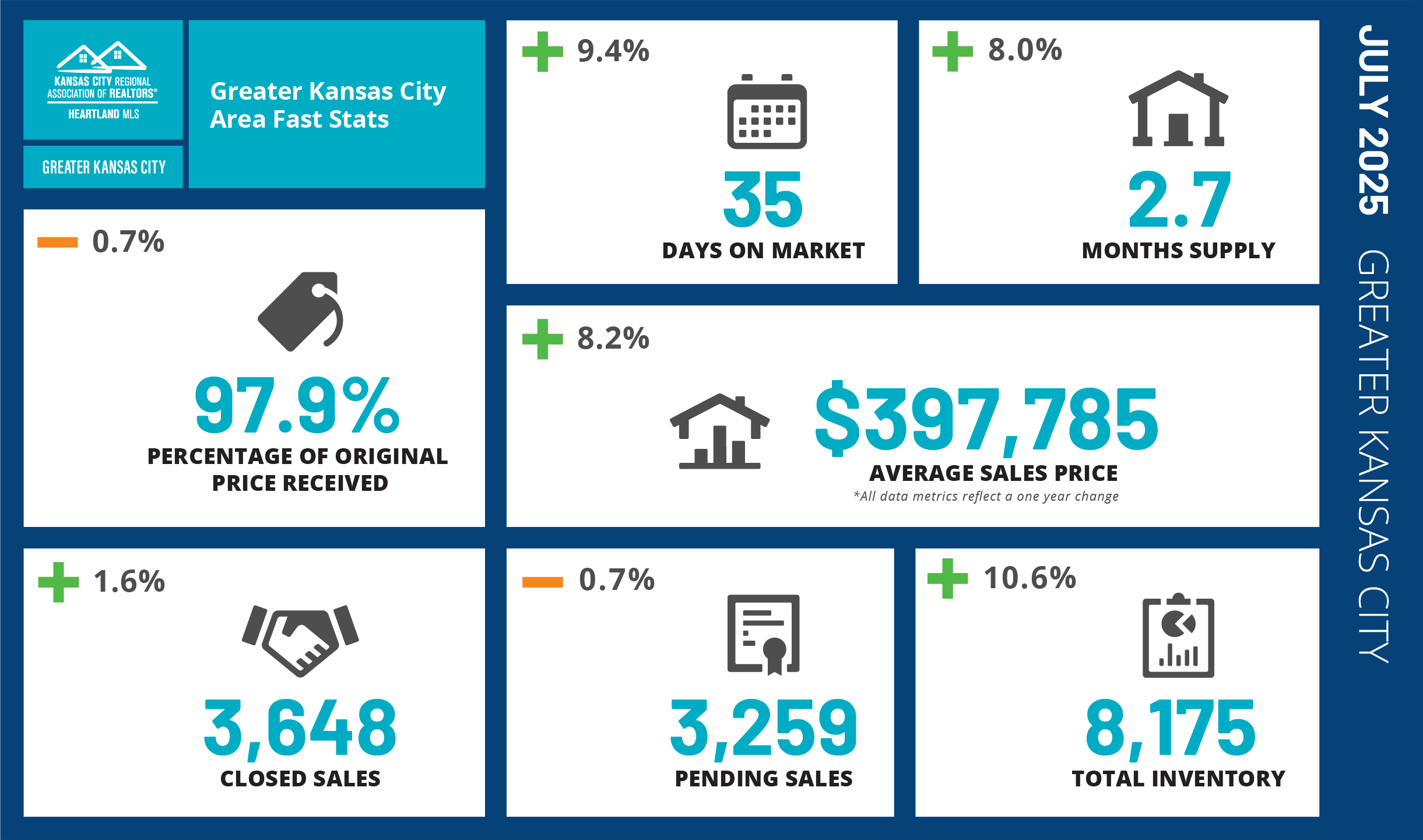

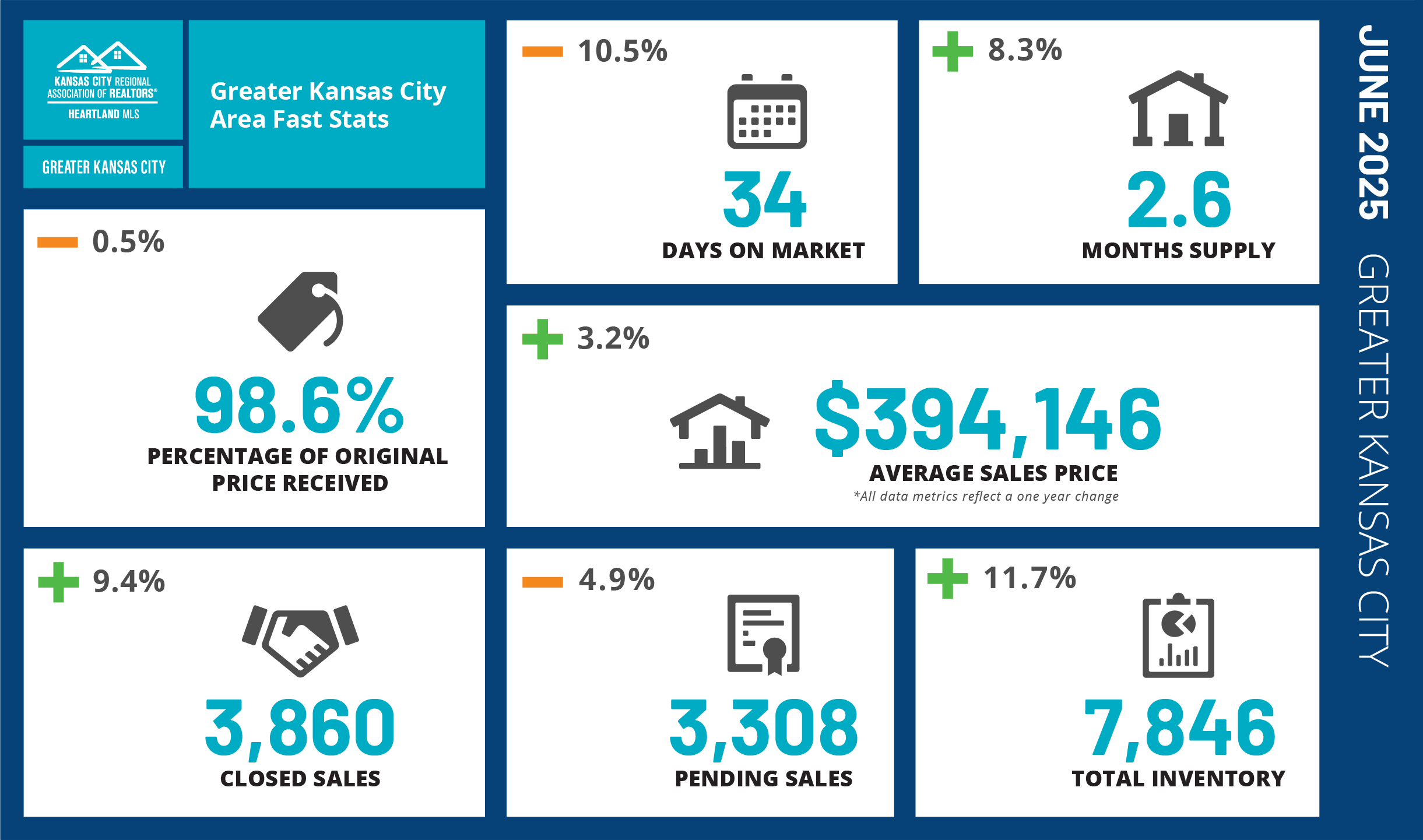

📊 Countywide Highlights

According to the latest data from the Heartland Multiple Listing Service, Q3 2025 showed notable gains in several key metrics compared to the same period last year:

-

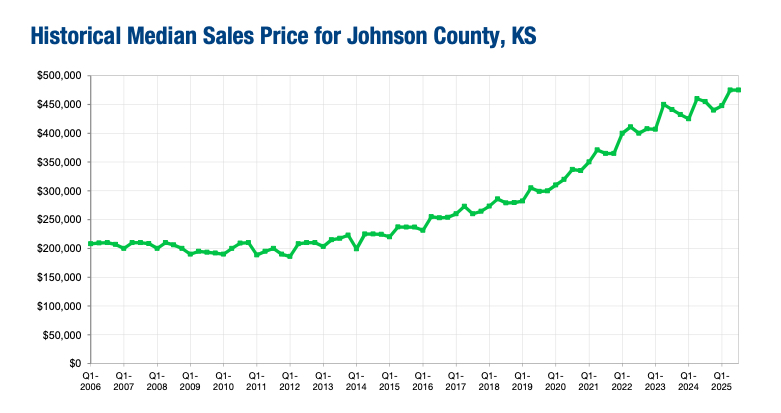

Median Sales Price: $475,000 (+4.4%)

-

Average Sales Price: $571,465 (+5.1%)

-

Closed Sales: 2,641 (+13.4%)

-

Active Inventory: 1,698 (+4.9%)

-

Days on Market: 32 (–5.9%)

-

Percent of Original Price Received: 99.5% (–0.8%)

-

Months of Supply: 2.2 (–8.3%)

Homes are still selling quickly and close to list price, showing that buyer demand remains strong and sellers are pricing their homes competitively.

🌟 Standout ZIP Codes

Several communities across Johnson County saw impressive growth this quarter:

-

66018 (De Soto): Median price jumped 33.1% to $398,500, paired with a strong 34% increase in average sales price.

-

66206 (Prairie Village): Average sales price climbed 34% to $970,262, underscoring continued demand for classic neighborhoods with charm and convenience.

-

66227 (Western Shawnee): Median price rose 13.6% to $633,350, with closed sales up over 40%, making it one of the county’s most active submarkets.

-

66013 (Southern Overland Park): Median price increased 16.5% to $700,000, fueled by steady new construction and high-end resale activity.

💬 What It Means for Buyers and Sellers

For sellers, the market remains favorable—homes that are well-presented and accurately priced continue to attract strong offers in a relatively short timeframe.

For buyers, there’s a bit more inventory to explore than last year, but competition is still present in most price ranges. Pre-approval and readiness to act quickly remain key advantages in securing the right home.

📈 Looking Ahead

Johnson County continues to set the pace for the greater Kansas City area, offering a stable and desirable market for homeowners and investors alike. With steady appreciation and consistent buyer activity, the local market is positioned for a confident finish to 2025.

Written by Gregory Weis, REALTOR® | Coldwell Banker Realty

Whether you’re thinking about buying, selling, or simply staying informed, I’m here to provide expert insight and guidance on the Kansas City real estate market.

📞 Let’s connect today to talk about your next move.

And more homes for sale means more choices. There’s a good chance your perfect match just hit the market – or it will soon. So, it’s a great time to explore what’s out there. As Jake Krimmel, Economist at Realtor.com, says:

And more homes for sale means more choices. There’s a good chance your perfect match just hit the market – or it will soon. So, it’s a great time to explore what’s out there. As Jake Krimmel, Economist at Realtor.com, says:

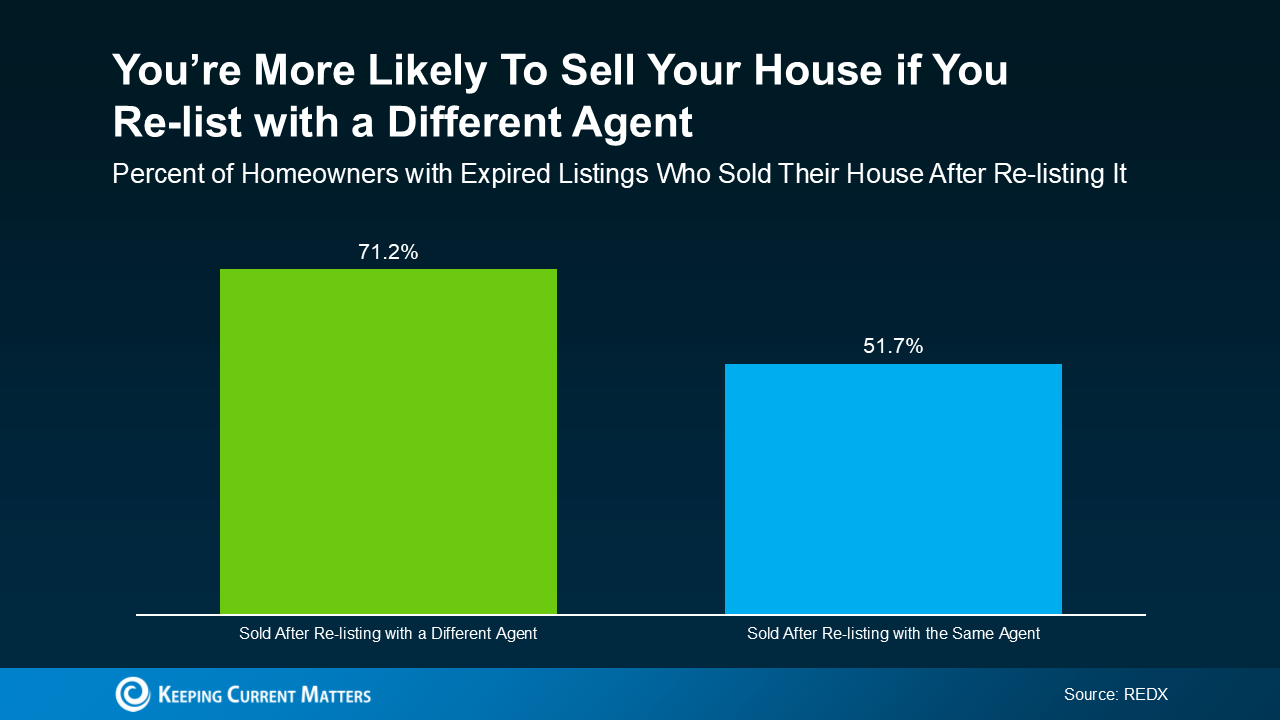

REDX data also shows that only 1 in 3 homeowners with expired listings actually make that change. That means most sellers either give up or repeat the same mistakes, so they get the same disappointing outcome. You deserve better.

REDX data also shows that only 1 in 3 homeowners with expired listings actually make that change. That means most sellers either give up or repeat the same mistakes, so they get the same disappointing outcome. You deserve better. 4. You Weren’t Willing To Negotiate

4. You Weren’t Willing To Negotiate